The Week in Review

Also available on YouTube:

This was a big week in the economic and financial fronts, hence this report might be a bit longer than usual.

News Highlights

Tensions in Iran

Iran said one of its ammunition depots was attacked in a drone strike. This happened while US Secretary of State Antony Blinken visited Israel. It’s not known who was behind the strike near the central city of Isfahan late Saturday and there’s been no official statement by Iran casting blame. But Tehran has often pointed the finger at Israel for similar incidents in the past.

The Wall Street Journal reported past Sunday that Israel was responsible, citing unnamed US officials and people familiar with the operation. The aim was to look for new ways to contain Tehran’s nuclear and military ambitions, the report said.

Goldman Says Risk to Oil Market From Iran Attack Limited For Now

The US and Israel are in agreement that Iran must not have nuclear weapons and are working together to counter the nation’s influence in the region, Blinken and Israeli Prime Minister Benjamin Netanyahu said in remarks to the press after meeting in Jerusalem on Monday.

“We discussed deepening cooperation to confront and counter Iran’s destabilizing activities,” Blinken said, adding that a further integration of Israel in the Middle East is also an aim. Neither he nor Netanyahu mentioned Saturday’s Iran attack in their statements.

(Source: https://news.yahoo.com/attack-iran-hikes-tensions-blinken-095612025.html)

World Health Organization and Nuclear Emergencies

On the 27th of January 2023, the World Health Organization (WHO) updated its list of medicines that should be stockpiled for radiological and nuclear emergencies, along with policy advice for their appropriate management. These stockpiles include medicines that either prevent or reduce exposure to radiation, or treat injuries once exposure has occurred.

“In radiation emergencies, people may be exposed to radiation at doses ranging from negligible to life-threatening. Governments need to make treatments available for those in need – fast,” said Dr Maria Neira, WHO Assistant Director-General a.i, Healthier Populations Division. “It is essential that governments are prepared to protect the health of populations and respond immediately to emergencies. This includes having ready supplies of lifesaving medicines that will reduce risks and treat injuries from radiation.”

Is the UK Heading into a Prolonged Recession?

This week the International Monetary Fund (IMF) became UK's public enemy number one for saying the UK will be the only rich economy to suffer a contraction in 2023. The BoE suspects the UK is headed for a 15 month long recession, culminating in 0.5 % and 0.25 % contractions this year and next, respectively.

IMF forecasters predict 0.6 % will be wiped off UK GDP this year, but most of that is on track to be recovered in 2024 when the economy grows nearly one per cent.

Adani Industries Slump

Gautam Adani, India’s top billionaire, had a good start of the year when he announced a follow-on public offer to raise capital from the Indian stock market. Troubles started mounting soon after a New York-based investment research firm by the name of Hindenburg Research published a report accusing Adani of potential fraud.

The report alleged that the Adani Group indulged in an accounting fraud and manipulation of stocks, a claim that has brought Adani down to his knees. After the release of the Hindenburg report, share prices of all of Adani Group’s companies fell drastically, a rout that has continued for six straight days. The Adani Group has lost up to $108 billion in a matter of a week.

At the moment, it is clear the Hindenburg report has opened the floodgates for the Adani Group to come clean on its balance sheet and shrug off allegations in all manners possible.

(Source: https://www.forbes.com/advisor/in/investing/why-adani-shares-are-falling/)

On The Economic Front

Economic Data Source: Trading Economics

Euro Area GDP Growth Rate YoY Flash

The Euro Area economy expanded 1.9% year-on-year in the last three months of 2022, below 2.3% in Q3 and the least since the covid-induced contractions in 2020 and early 2021, but above market forecasts of 1.8%, according to preliminary estimates. Ireland recorded the biggest growth rate (15.7%), followed by Portugal (3.1%), Spain (2.7%) and Austria (2.7%). Considering the biggest economies, Germany expanded 1.1%, France 0.5% and Italy 0.1%. Considering full 2022, the Eurozone GDP expanded 3.5%.

Germany GDP Annual Growth Rate

Germany's annual economic growth slowed to 1.1 percent in the fourth quarter of 2022, down from a revised 1.4 percent in the previous three-month period and below market expectations of 1.3 percent, a preliminary estimate showed. Europe's largest economy was hit by rising interest rates, stubbornly high inflation, and supply chain bottlenecks.

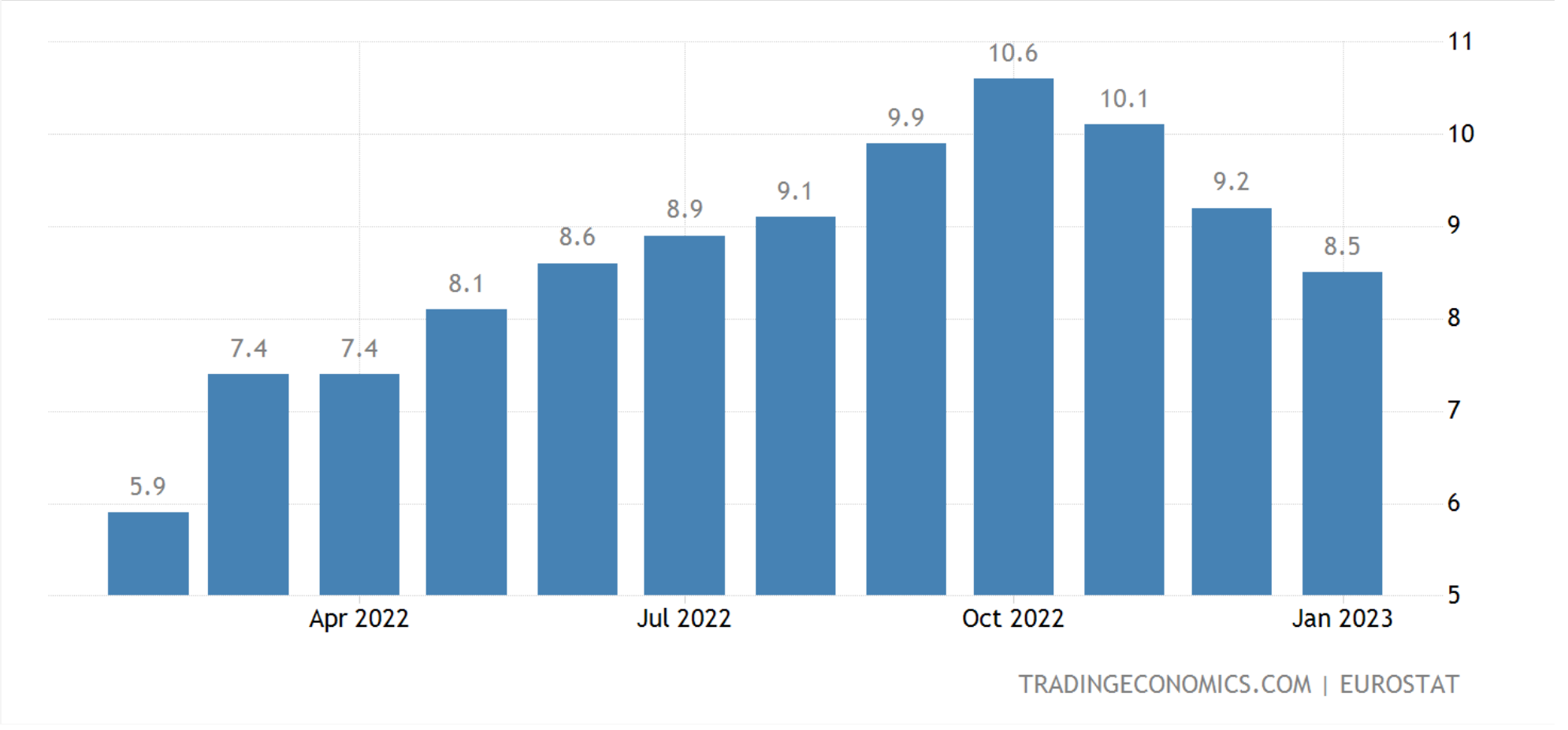

Euro Area Inflation Rate (YoY)

Annual inflation rate in the Euro Area fell to an eight-month low of 8.5% in January of 2023 from 9.2% in December, below forecasts of 9%, preliminary estimates showed. The data for Germany inflation is not available though, as the country's statistical office had to delay the release of its own figures due to technical issues with data processing. Inflation slowed in Italy, Ireland and the Netherlands, but edged higher in Spain and France.

Also, core inflation which excludes prices of energy, food, alcohol and tobacco remained steady at 5.2%, adding to further evidence that price pressures remained elevated in the bloc's economy. Energy prices rose at a slower pace (17.2% vs 25.5%) and services inflation also eased (4.2% vs 4.4%) while cost increased faster for food, alcohol & tobacco (14.1% vs 13.8%) and non-energy industrial goods (6.9% vs 6.4%). Compared to the previous month, consumer prices fell 0.4%, the same as in December, led by a 0.9% decline in energy cost.

Euro Area Unemployment Rate

The euro area seasonally-adjusted unemployment rate was 6.6 percent in December 2022, stable compared with November 2022 and above market forecasts of 6.5%. A year earlier, the jobless rate was higher at 7.0%. The number of unemployed increased by 23 thousand from a month earlier to 11.048 million. Meanwhile, the youth unemployment rate, measuring job-seekers under 25 years old, was unchanged at 14.8 percent. Amongst the largest Euro Area economies, the highest jobless rates were recorded in Spain (13.1 percent), Italy (7.8 percent) and France (7.1 percent), while the lowest rates were recorded in Germany (2.9 percent).

United States ISM Purchasing Managers Index (PMI)

The ISM Manufacturing PMI fell to 47.4 in January, the lowest since May 2020 at the height of the covid pandemic and below market forecasts of 48. The reading pointed to the third consecutive contraction in factory activity as companies slowed outputs to better match demand in the first half of 2023 and prepare for growth in the second half of the year. Further declines were seen for new orders (42.5 vs 45.1), production (48 vs 48.6) and backlogs of orders (43.4 vs 41.4) while inventories (50.2 vs 52.3) slowed, the supplier deliveries index indicated faster deliveries (45.6 vs 45.1) and the price index increased (44.5 vs 39.4). At the same time, employment (50.6 vs 50.8) rose slightly less but companies are indicating that they are not going to substantially reduce headcounts as they are positive about the second half of the year.

United States Job Openings

The number of job openings in the United States increased to 11.0 million in December of 2022, the most in 5 months and above market expectations of 10.25 million. Over the month, the largest increases were in accommodation and food services (+409,000), retail trade (+134,000), and construction (+82,000). On the other hand, the number of available positions decreased in information (-107,000). Meanwhile, the number of hires and total separations changed little at 6.2 million and 5.9 million, respectively. Within separations, quits (4.1 million) and layoffs and discharges (1.5 million) changed little. The ratio of openings to unemployed people rose to a near record-high 1.9 from 1.7 a month earlier and compared to 1.2 before the pandemic.

United States Fed Funds Rate

On Wednesday, we had the so awaited fed funds rate decision and press conference. The Federal Reserve raised the target range for the fed funds rate by 25bps to 4.5%-4.75% in its February 2023 meeting, dialing back the size of the increase for a second straight meeting, but still pushing borrowing costs to the highest since 2007. The decision came in line with market expectations. Policymakers added that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2%. During the regular press conference, Chair Powell reinforced the disinflation process is on an early stage and that interest rates are not yet at a sufficiently restrictive level. In determining the size of future rate increases, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

Euro Area Interest Rate

The European Central Bank raised the interest rate on the main refinancing operations by 50 bps to 3.0 % during its February meeting, pushing up borrowing costs to the highest level since late 2008 and pledging to deliver another 50 bps rate hike at its next monetary policy meeting in March. The central bank has also reaffirmed it would stay the course in raising rates significantly at a steady pace and in keeping them at levels that are sufficiently restrictive to ensure a timely return of inflation to its 2% medium-term target. Moreover, officials announced the APP portfolio would decline by €15 billion per month on average from the beginning of March until the end of June 2023, and the subsequent pace of portfolio reduction would be determined over time. The interest rates on the marginal lending facility and the deposit facility were also increased to 3.25 percent and 2.50 percent respectively.

A Walk Around the Markets

The Dow closed more than 100 points lower on Friday, and the S&P 500 and Nasdaq 100 dipped in negative territory by 1% and 1.6%, respectively, as strong job reports signaled that the Fed will continue its tightening cycle pushing rates above 5%. The Labor Department's closely watched employment report showed that US employers hired more workers than expected in January, with nonfarm payrolls increasing by 517,000 jobs last month. On top of that, ISM data showed that the services sector, which accounts for more than two-thirds of US economic activity, rebounded sharply in January. Traders also digested disappointing earning results from Alphabet (-2.7%), and Amazon (-8.4%) that dragged them down, while Apple rebounded from early losses and finished 2.4% higher. For the week, the Nasdaq 100 rallied 4.1%, marked the fifth consecutive weekly gain. The S&P 500 added almost 2% and posted second straight weekly gain, while the Dow lost 0.1%.

Source: Trading Economics

On Friday, silver futures traded around the $23 per ounce level, not seen since mid-January. Still, projections of weak supply limited the fall, as COMEX inventories remained under pressure and LBMA stockpiles plunged amid outflows to India.

Source: Goldmoney, Alasdair Macleod

After trading sideways until Wednesday,

gold broke out above its recent consolidation level following the Fed’s

0.25% rate increase on Wednesday. Thursday morning, gold rose

briefly to $1959.7 before falling back to $1911. Given the recent price action, it could suggest

that gold is temporarily overbought. But looking at Open Interest on

Comex, this is far from the case. Open interest is the total number of contracts outstanding between market participants, in this case in the COMEX market (futures market).

Looking at the managed money, this shows that while the gold price has increased significantly, net Managed Money positions have less so. Bearing in mind that the long-term average net long position is 110,000 contracts, currently gold is marginally oversold.

Physical supplies are extremely tight, with central banks still buying, and one supposes that governments are also accumulating bullion in addition to physical reserves. Some coins are in very short supply. Anecdotal evidence in London is that sovereigns are extremely scarce with some dealers sold out. In Germany members of the public are buying gold in significant quantities as well. And deliveries on Comex this week alone have reached 11,817 contracts (36.75 tonnes).

We can conclude that while there could be some short-term downside in paper markets, with good solid underlying physical demand, gold appears to be in the early stages of a bullish move and any reaction in the price is likely to be very limited.

If we regard gold as true money and dollars as fiat credit, we understand that gold is not in a bull market. It is the fiat dollar which is losing purchasing power.

Opinion Section

The interest rate decisions of the US and EU central banks didn't surprise. Economic indicators start showing more and more subtle signs of a slowing economy, although the labor markets continue tight. The scenarios of a soft landing versus a hard landing are still unclear and the effects of monetary policy tightening will only be seen later in the year. Investors need to be patient and cautious, a difficult combination.

The earnings season is still not over, but some softening can be seen in earnings. Very optimistic growth projections for the near future must be taken with a grain of salt. We might not have a stock market crash, maybe only a slow adjustment of valuations as the year unfolds and waves of optimism and pessimism come and go.

In the geopolitical front, namely in Ukraine, there is no end in sight for the conflict, and thoughts of an escalation of the conflict are disturbing, to say the least.

Upcoming

Next week, in the US, earnings reports, Michigan consumer confidence, and trade balance data will take the spotlight. Also, the focus will be on central bank meetings in Australia and India and inflation data in Germany, China, Brazil, Mexico, Russia, and the Philippines.

Have a nice week.

Comments

Post a Comment